Creating precisely targeted email audiences is essential for InsurTech carriers and Managing General Agents (MGAs) competing in today's digital marketplace. Generic mass emails no longer cut it—insurance buyers expect personalized communications that address their specific risk profiles, coverage needs, and lifecycle stage. Multi-layer email audience segmentation combines firmographic, technographic, behavioral, and intent data to deliver highly relevant messaging that drives materially higher conversion rates compared to unsegmented campaigns. By leveraging advanced audience discovery tools like natural-language targeting platforms, insurance marketers can build AI-qualified prospect lists more efficiently than manual research.

The most effective approach starts with foundational segments based on company characteristics and policy types, then layers on digital behavior, technology adoption signals, and market triggers to create composite profiles of ideal prospects. This systematic method enables InsurTech teams to move beyond basic demographic assumptions and engage prospects when they're most receptive to new coverage solutions.

Key Takeaways

- Multi-layer segmentation combines firmographic, technographic, behavioral, and intent data to create precise insurance buyer profiles

- Start with a handful of foundational segments based on policy types and lifecycle stages before adding complexity

- Event-based triggers like policy renewals and funding rounds generate significantly higher engagement than static campaigns

- AI-powered audience discovery platforms can accelerate qualified prospect list-building using natural language prompts

- Proper data hygiene and validation are essential for maintaining segment accuracy and email deliverability

What Is Segmentation and Why It Matters for InsurTech

Customer segmentation in insurance involves dividing your audience into distinct groups based on shared characteristics that influence their insurance needs, buying behavior, and risk profile. Unlike basic demographic segmentation, multi-layer approaches consider multiple dimensions simultaneously to create nuanced profiles that accurately predict policy interest and renewal likelihood.

For InsurTech carriers and MGAs, sophisticated segmentation directly impacts bottom-line metrics. Insurance companies using advanced segmentation strategies report higher policy retention rates and significantly improved cross-sell conversion. The difference between single-variable and multi-layer segmentation is substantial—while targeting only company size might identify potential commercial insurance buyers, combining size with technology stack, hiring patterns, and geographic risk factors reveals which prospects are actively evaluating new coverage options.

Core Segmentation Principles for Insurance

Effective insurance segmentation must account for the unique characteristics of the industry, including long sales cycles, complex buying committees, and regulatory constraints. Key principles include:

- Risk-based grouping: Segment by risk profiles and coverage gaps rather than just company attributes

- Lifecycle alignment: Match messaging to where prospects are in their buying journey (research, evaluation, renewal)

- Compliance awareness: Ensure segmentation variables comply with insurance regulations and email privacy laws including CAN-SPAM, GDPR, and CCPA

- Behavioral emphasis: Prioritize observed behaviors over demographic assumptions when possible

The Difference Between Single-Variable and Multi-Layer Segmentation

Single-variable segmentation might target "manufacturing companies with 50-200 employees," while multi-layer segmentation would identify "manufacturing companies with 50-200 employees in tornado-prone regions that recently hired risk management staff and are using legacy policy administration systems." The latter approach captures not just who the prospect is, but their current needs, readiness to buy, and specific pain points.

Customer Segmentation Examples Specific to InsurTech and MGAs

Insurance-specific segmentation requires understanding both personal and commercial lines differences, as well as the unique dynamics of MGA operations. Here are concrete examples that drive measurable results:

- High-value commercial accounts: Companies with $10M+ revenue in industries with high liability exposure (construction, transportation) that have filed multiple claims in the past 24 months—prime candidates for enhanced coverage packages

- Renewal risk segments: Policyholders approaching renewal who have reduced website engagement and haven't interacted with renewal communications—indicating potential lapse risk requiring proactive retention outreach

- Digital transformation prospects: MGAs using legacy policy admin systems who have posted job openings for IT or digital transformation roles—signaling readiness to evaluate modern insurance technology solutions

- Geographic risk zones: Personal lines customers in areas recently affected by natural disasters who may need coverage adjustments or additional protection

- Commercial vs. personal lines: Separate segmentation strategies for business insurance (firmographic focus) versus individual policies (demographic and life-stage focus)

Segmenting by Policy Type and Coverage Level

Different insurance products require distinct segmentation approaches. Commercial property insurance prospects need different targeting criteria than cyber liability or workers' compensation buyers. Segment by:

- Current policy types held

- Coverage limits and deductibles

- Policy bundling patterns

- Claims frequency and severity

- Industry-specific risk factors

Behavioral Segments: Engagement, Renewal Propensity, and Claims History

Behavioral data often provides the most accurate segmentation signals in insurance. Track:

- Email open and click patterns on policy-related content

- Website visits to specific coverage pages

- Quote request abandonment rates

- Claims submission frequency and types

- Customer portal login activity

Layer 1: Firmographic and Demographic Segmentation

Firmographic segmentation forms the foundation of commercial insurance targeting, while demographic data drives personal lines strategies. Key variables include:

- Company size (employee count, revenue bands)

- Industry classification (NAICS/SIC codes)

- Geographic location (state, region, risk zones)

- Years in operation

- Business structure (LLC, corporation, partnership)

For personal lines, demographic variables like age, income level, homeownership status, and family composition are more relevant.

Key Firmographic Signals for Commercial Insurance Buyers

The most predictive firmographic signals for commercial insurance include:

- Industry vertical: Different sectors have distinct risk profiles and coverage needs

- Employee count: Correlates with workers' compensation and group benefits requirements

- Revenue bands: Indicates financial capacity and potential policy size

- Geographic location: Determines exposure to weather-related and regulatory risks

- Years in business: Startups often need different coverage than established companies

Demographic Variables for Personal Lines

For individual policyholders, focus on:

- Age and life stage (young professional, family with children, retiree)

- Income and asset levels

- Homeownership vs. rental status

- Vehicle ownership and types

- Geographic location and associated risks

Layer 2: Technographic and Digital Maturity Signals

Technology adoption patterns reveal insurance buyers' digital maturity and readiness to evaluate new solutions. Companies using legacy systems may be prime prospects for modern insurance platforms, while those already using advanced tech might need specialized add-on coverage.

Key technographic signals include:

- Policy administration system (legacy vs. modern cloud platforms)

- CRM adoption and integration capabilities

- Digital self-service portal usage

- Mobile app engagement levels

- API integration requirements

Identifying Prospects by Technology Stack

Insurance technology stacks provide valuable insights into prospects' operational maturity and potential pain points. Companies using outdated systems often struggle with:

- Manual underwriting processes

- Poor customer experience

- Limited data analytics capabilities

- Integration challenges with modern tools

- Compliance and security vulnerabilities

Targeting Based on Digital Self-Service Behavior

Digital engagement patterns reveal which prospects value self-service capabilities and might respond well to modern insurance platforms. Track:

- Online quote completion rates

- Customer portal feature usage

- Mobile app download and retention rates

- Digital document signing preferences

- Online payment adoption

Layer 3: Behavioral and Engagement Segmentation

Behavioral segmentation captures how prospects and policyholders actually interact with your brand, providing real-time signals of interest and intent. This layer is particularly powerful for timing outreach and personalizing messaging.

Key behavioral signals include:

- Website visit frequency and page views

- Email engagement (opens, clicks, forwards)

- Content downloads (whitepapers, case studies)

- Quote requests and form completions

- Customer service interactions

Tracking Prospect and Policyholder Engagement

Effective behavioral tracking requires consistent data collection across touchpoints:

- Website analytics with visitor identification

- Email marketing platform engagement metrics

- CRM interaction history

- Customer portal activity logs

- Call center interaction records

Building High-Intent Segments from Web Behavior

High-intent behavioral segments include:

- Visitors who viewed pricing pages multiple times

- Users who downloaded product comparison guides

- Prospects who abandoned quote forms near completion

- Policyholders who researched additional coverage options

- Visitors who spent significant time on specific policy pages

Layer 4: Intent and Market Trigger Segmentation

Intent signals and market triggers identify prospects at optimal buying moments, often before they've actively researched solutions. These external indicators reveal when companies are most likely to evaluate new insurance coverage.

Key intent and trigger signals include:

- Funding events (venture capital rounds, debt financing)

- M&A activity (acquisitions, mergers, divestitures)

- Job postings (especially for risk management, IT, or finance roles)

- Regulatory changes affecting specific industries

- Industry conference attendance

- Geographic expansion or new location openings

- Competitive wins or losses

Using Hiring Signals to Identify Growth-Stage Prospects

Hiring patterns provide powerful intent signals for insurance buyers:

- Risk management role postings indicate active evaluation of coverage needs

- IT and digital transformation hires suggest technology platform evaluation

- Finance and accounting role expansions may signal growth requiring increased coverage

- Executive leadership changes often trigger comprehensive policy reviews

Triggering Outreach Based on Funding and Expansion

Funding events and expansion activities create immediate insurance needs:

- Series A+ funding rounds often require enhanced D&O and cyber liability coverage

- Geographic expansion necessitates additional location-specific policies

- M&A activity creates complex integration and coverage gap challenges

- New product launches may require specialized liability coverage

Combining Layers: Building Composite Audience Profiles

The real power of multi-layer segmentation emerges when you combine multiple data dimensions to create precise composite profiles. This approach moves beyond simple attribute stacking to create nuanced understanding of ideal prospects.

Effective composite profile construction involves:

- Start with firmographics: Establish baseline targeting (industry, size, location)

- Add technographics: Layer on technology adoption and digital maturity signals

- Incorporate behavioral data: Include engagement patterns and interaction history

- Apply intent triggers: Time outreach based on market events and buying signals

- Exclude irrelevant segments: Remove prospects who don't meet minimum criteria

How to Stack Firmographic, Technographic, and Intent Layers

For example, an ideal commercial cyber insurance prospect might be:

- Firmographic: Technology company with 100-500 employees, $10M-$50M revenue

- Technographic: Uses cloud infrastructure but lacks modern security platforms

- Behavioral: Visited cyber insurance pages and downloaded security whitepapers

- Intent: Recently raised Series B funding and hired CISO

This composite profile is far more precise than any single-layer approach and enables highly relevant messaging.

Practical Example: Targeting Mid-Market MGAs Adopting New Tech

A composite profile for MGAs evaluating new policy admin systems might include:

- Firmographic: MGA with 50-200 employees serving commercial clients

- Technographic: Using legacy policy admin system, limited API integrations

- Behavioral: Engaged with digital transformation content, attended webinars

- Intent: Posted job openings for IT transformation roles, attended InsurTech conferences

Segmentation for Renewal Campaigns vs New Business Acquisition

Renewal and acquisition campaigns require distinct segmentation strategies, as the objectives, messaging, and timing differ significantly.

Tailoring Messaging for Renewal Segments

Renewal segmentation should focus on:

- Policyholder tenure and historical engagement

- Claims history and risk profile changes

- Coverage gaps identified during policy term

- Competitive threats (similar policies offered by competitors)

- Renewal risk scores based on behavioral indicators

Renewal messaging should emphasize continuity, relationship value, and enhanced coverage options rather than introductory offers.

Building Net-New Prospect Segments for Commercial Lines

New business acquisition segments should prioritize:

- Growth indicators (hiring, funding, expansion)

- Technology adoption signals (legacy system usage, digital transformation)

- Industry-specific risk factors (regulatory changes, market conditions)

- Competitive displacement opportunities (prospects using inferior solutions)

- Buying committee formation (new executive hires, role changes)

Acquisition messaging should focus on pain point resolution, competitive advantages, and implementation ease.

Data Quality and Hygiene for Multi-Layer Segmentation

Data quality directly impacts segmentation effectiveness. Poor data hygiene leads to misdirected communications, wasted resources, and damaged brand reputation.

Key data quality considerations include:

- Contact validation: Ensure email addresses and phone numbers are current

- Duplicate removal: Eliminate redundant records across data sources

- Data standardization: Apply consistent formatting and categorization

- Regular refresh cycles: Update firmographic and technographic data quarterly

- Suppression list management: Respect opt-outs and compliance requirements

Ensuring Accurate Contact Data Across Segments

Contact data accuracy is particularly critical for email deliverability and compliance:

- Email verification: Validate addresses before campaign deployment

- Phone validation: Confirm numbers are active and correctly formatted

- Role verification: Ensure job titles and responsibilities are current

- Company verification: Confirm businesses are still operating and haven't merged

Managing Data Decay in Insurance Audiences

Insurance data decays rapidly—many insurance companies struggle with data quality issues that undermine segmentation accuracy. Implement processes to:

- Monitor engagement metrics: Flag inactive contacts for revalidation

- Track bounce rates: Remove invalid email addresses automatically

- Leverage third-party enrichment: Supplement internal data with verified external sources

- Establish data governance policies: Define ownership and maintenance responsibilities

Activation: Turning Segments into Personalized Email Campaigns

Effective activation transforms sophisticated segments into compelling email campaigns that drive measurable results.

Key activation best practices include:

- Dynamic content: Tailor email copy and offers based on segment attributes

- Personalized subject lines: Increase open rates with relevant messaging

- Segment-specific CTAs: Align calls-to-action with prospect needs and lifecycle stage

- Multi-channel coordination: Extend segmented messaging across email, web, and social

- A/B testing: Continuously optimize messaging based on segment performance

Mapping Segment Attributes to Email Content

For each segment, develop content that addresses specific needs:

- Growth-stage prospects: Focus on scalability and implementation speed

- Renewal-risk policyholders: Emphasize relationship value and enhanced coverage

- Technology evaluation prospects: Highlight integration capabilities and ROI

- High-risk segments: Address specific coverage gaps and risk mitigation

Testing and Iterating on Segment Performance

Continuous optimization is essential for maximizing segmentation ROI:

- Track segment-level metrics: Monitor open rates, click-through rates, and conversions by segment

- Conduct A/B tests: Test different messaging approaches within segments

- Refine segment definitions: Adjust criteria based on performance data

- Expand successful segments: Scale high-performing segments while sunsetting underperformers

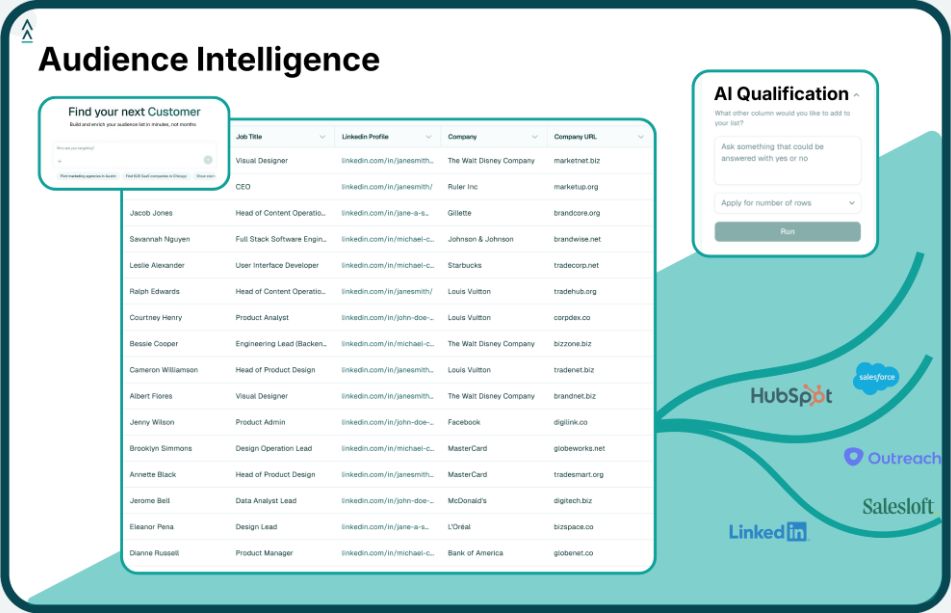

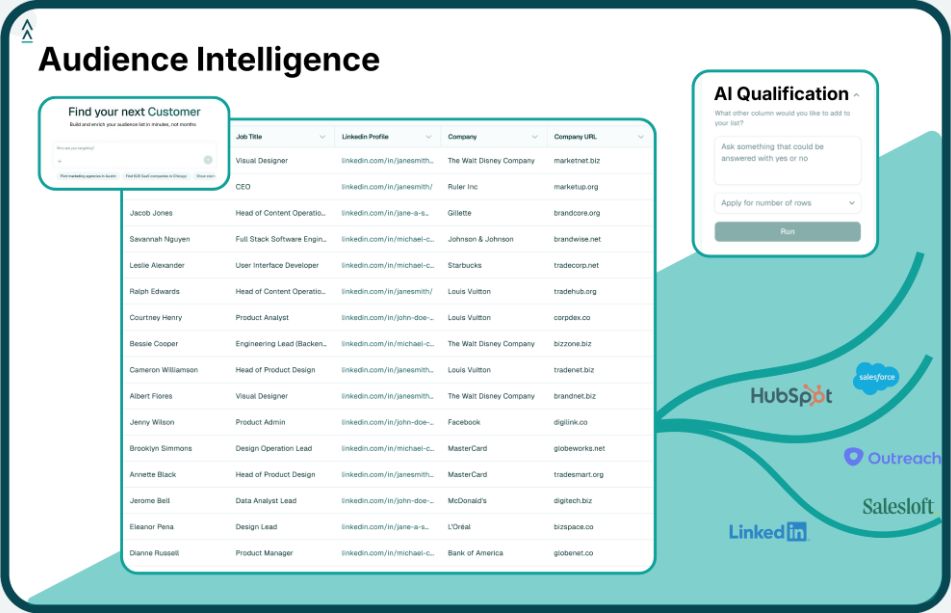

Landbase: AI-Powered Audience Discovery for InsurTech Teams

For InsurTech carriers and MGAs looking to implement sophisticated multi-layer segmentation without extensive manual research, Landbase offers a streamlined solution. The platform's core value lies in its ability to accelerate audience discovery using natural language prompts, eliminating extensive manual data gathering and filtering.

Landbase's GTM-2 Omni agentic AI engine interprets plain-English queries like "MGAs with 100-500 employees using legacy policy systems and hiring for digital transformation roles" and generates qualified prospect lists. The platform leverages hundreds of unique signals including firmographic, technographic, behavioral, and intent data to ensure audience precision.

Key benefits for InsurTech teams include:

- Streamlined audience building: Access via VibeGTM interface

- AI Qualification: Both online and offline qualification ensures high-quality prospects

- Efficient exports: Download contacts for immediate campaign activation

- Dynamic signal layer: Data enrichment ensures audiences reflect current market conditions

- Natural-language targeting: Eliminates complex filtering interfaces and technical setup

Rather than piecing together data from multiple sources or spending hours building complex database queries, InsurTech marketers can leverage Landbase's agentic AI to focus on what they do best—creating compelling messaging and building relationships with qualified prospects.

Measuring Segmentation Performance and Iterating

Effective segmentation requires continuous measurement and refinement to maintain relevance and drive ROI.

Key performance metrics to track include:

- Conversion rates: Quote requests, policy applications, and renewals by segment

- Segment lift: Performance improvement compared to unsegmented campaigns

- Engagement metrics: Open rates, click-through rates, and content interaction

- ROI by segment: Revenue generated versus campaign costs for each segment

- Retention by cohort: Policy renewal rates for different customer segments

Key Metrics for Evaluating Segment Quality

High-quality segments should demonstrate:

- Consistent performance: Stable conversion rates over time

- Actionable size: Large enough to generate meaningful results but specific enough to be relevant

- Clear differentiation: Distinct performance patterns compared to other segments

- Predictive accuracy: Ability to identify prospects likely to convert or renew

Using Performance Data to Refine Audience Layers

Regular segment review should include:

- Quarterly performance analysis: Identify top-performing and underperforming segments

- Data source evaluation: Assess which signals provide the most predictive value

- Segment consolidation: Merge segments with similar performance characteristics

- New segment creation: Develop segments based on emerging market trends or customer behaviors

- Exclusion rule refinement: Improve targeting by removing unresponsive prospects

Frequently Asked Questions

What is the difference between single-layer and multi-layer segmentation for InsurTech?

Single-layer segmentation uses one data dimension (like company size or industry), while multi-layer segmentation combines firmographic, technographic, behavioral, and intent signals to create composite profiles. Multi-layer approaches achieve significantly higher conversion rates because they capture both who prospects are and their current buying readiness. This precision enables InsurTech teams to deliver more relevant messaging at optimal moments in the buyer journey.

How do firmographic and technographic signals work together in audience building?

Firmographics establish the baseline targeting (industry, size, location), while technographics reveal digital maturity and potential pain points. For example, targeting manufacturing companies (firmographic) that use legacy policy admin systems (technographic) identifies prospects likely to need modern insurance technology solutions. Together, these layers create a more complete picture of both prospect fit and readiness to buy.

What are the best customer segmentation examples for MGAs selling commercial insurance?

Effective MGA segments include companies with recent funding rounds requiring enhanced coverage, businesses in high-risk geographic areas needing specialized policies, firms hiring risk management staff indicating active evaluation, and organizations using outdated technology platforms ready for digital transformation. Each segment combines multiple data layers to identify prospects with specific coverage needs and buying signals.

How often should InsurTech carriers refresh and re-segment their email audiences?

Firmographic and technographic data should be refreshed quarterly, behavioral scoring updated monthly, and segment performance reviewed quarterly. Most carriers see measurable improvement within several months of implementing segmented campaigns. Regular refresh cycles ensure your segments remain accurate as prospect characteristics and behaviors evolve.

What data sources are needed to build intent-based segments for insurance buyers?

Intent-based segments require external data sources tracking funding events, job postings, M&A activity, industry conference attendance, and regulatory changes. Platforms like Landbase aggregate these signals across hundreds of unique data points to identify prospects at optimal buying moments. Combining intent signals with firmographic and behavioral data creates highly precise targeting that improves campaign performance.

How can behavioral segmentation improve renewal rates for insurance policies?

Behavioral segmentation identifies at-risk policyholders through reduced engagement patterns (email opens, website visits, portal logins) 60-90 days before renewal. Targeted retention campaigns to these segments can materially reduce policy cancellation rates through proactive outreach and personalized offers. By monitoring engagement signals, insurers can intervene before policyholders have fully decided to switch carriers.

.png)

.png)