.png)

.png)

Daniel Saks

Chief Executive Officer

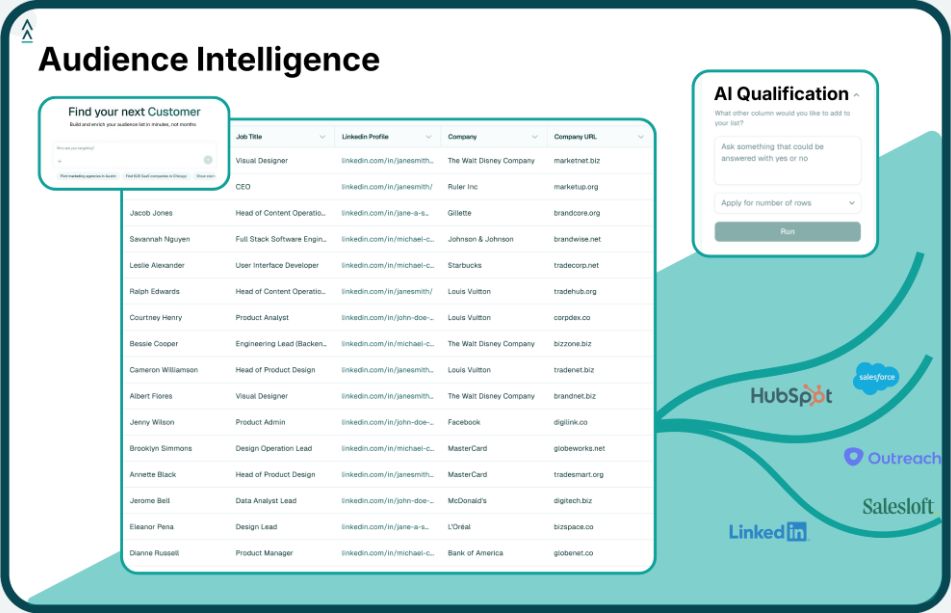

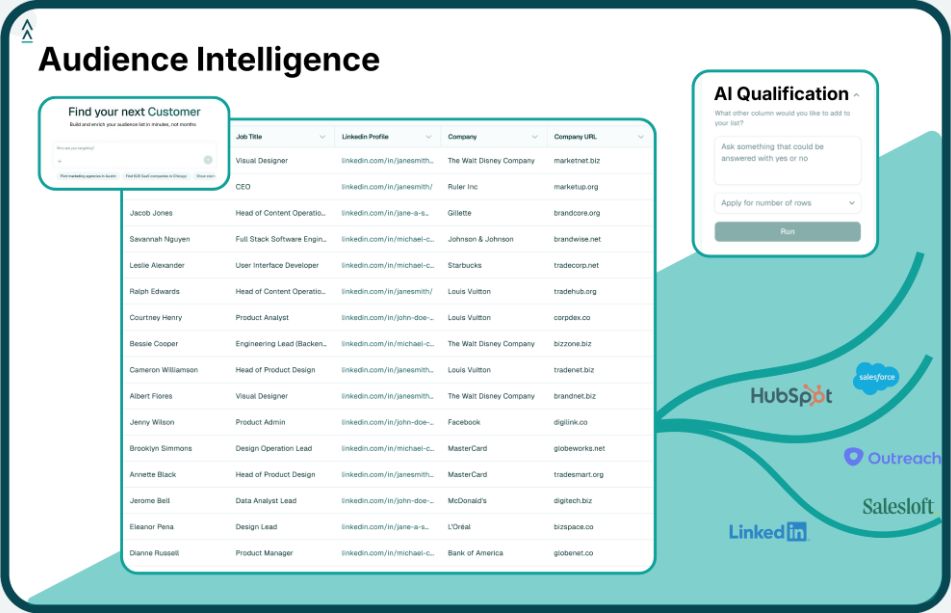

The global neobanking market is experiencing unprecedented growth, projected to reach $7.6 billion by 2034 with a 49.3% annual growth rate. These digital-first banks are revolutionizing financial services by targeting specific customer segments with precision, much like how modern B2B companies identify their ideal customers. For go-to-market teams in financial services and adjacent industries, understanding which neobanks are leading this transformation is crucial. Platforms like Landbase's AI-qualified audience discovery now enable companies to identify decision-makers at these fast-growing fintechs using natural-language prompts like "CFOs at Series B neobanks with 1M+ customers."

Nubank is the world's largest neobank by customer count, serving over 125 million customers across Latin America with digital banking, credit cards, and investment products. Founded in 2013, the company pioneered financial inclusion in Brazil by providing banking services to traditionally underbanked populations through innovative mobile-first technology and alternative credit scoring models.

Nubank represents the ultimate proof point that neobanks can achieve both massive scale and sustainable profitability. Its focus on financial inclusion has brought millions of previously unbanked Latin Americans into the formal financial system, transforming the region's banking landscape while generating exceptional financial returns. The company's success validates that emerging market fintech can compete globally while solving critical infrastructure gaps.

Publicly traded on NYSE (NU). As a public company, Nubank raises capital through public equity markets rather than venture funding rounds.

Revolut operates as a financial super-app, combining banking, cryptocurrency trading, stock investing, and international money transfers in a single platform. With operations in 40+ countries and 52.5 million customers, the London-based company has evolved from a simple currency exchange app into a comprehensive financial services platform targeting globally mobile consumers and businesses.

Revolut demonstrates how a super-app strategy can create sticky customer relationships and diversified revenue streams. By integrating multiple financial services into one platform, the company reduces customer churn while increasing lifetime value, setting a new standard for neobank business models. Four consecutive years of profitability prove the viability of this approach at scale.

Maintains $75 billion private valuation; has not raised external funding recently due to profitability and strong cash flow from operations.

Chime is the largest US neobank, serving 22.3 million customers with fee-free banking, early paycheck access, and overdraft protection through its SpotMe feature. The San Francisco-based company pioneered the fee-free banking model in the US, eliminating monthly fees, overdraft charges, and minimum balance requirements that plague traditional banks.

Chime has proven that the fee-free banking model can achieve massive scale in the US market. By eliminating traditional banking fees and providing features like early paycheck access, the company has captured significant market share from traditional banks while building a loyal customer base of millennials and Gen Z consumers. Its confidential IPO filing signals maturation of the US neobank sector.

Confidential IPO filing in December 2024 with plans for 2025 public listing. Previously raised $2.65 billion in venture funding.

Mercury specializes in banking services for startups, serving over 100,000 early-stage companies with business accounts, treasury management, and credit tools. The San Francisco-based company has built a comprehensive banking platform specifically designed for the unique needs of startups, including venture debt, expense management, and fundraising support.

Mercury exemplifies how vertical specialization can drive explosive growth in financial services. By focusing exclusively on startups—a segment often underserved by traditional banks—the company has built deep product expertise and customer loyalty that translates into exceptional revenue growth and market positioning. Its $500M ARR from a focused market demonstrates the power of niche dominance.

Series B: $120 million+ raised. Currently in talks for new round at $3+ billion valuation with Sequoia Capital leading.

Monzo is a UK-based consumer neobank serving 12 million customers with mobile-first banking, budgeting tools, and financial wellness features. Known for its distinctive coral-colored cards and innovative features like instant spending notifications and shared tabs for bill splitting, Monzo has built a loyal customer base focused on financial transparency and control.

Monzo proves that UK neobanks can achieve sustainable profitability while maintaining customer growth. The company's focus on financial wellness and transparent pricing has resonated with UK consumers, while its strategic expansion into mortgages (Habito acquisition) and international markets positions it for continued growth beyond basic banking services.

Series: $190 million raised (May 2024) at $5.9 billion valuation from Hedosophia and CapitalG (Alphabet).

Current focuses on youth and family banking, serving 4 million customers with teen banking solutions, instant refunds on gas station holds, and points rewards on debit purchases. The New York-based company has built a comprehensive platform for young Americans and families seeking modern banking alternatives to traditional institutions.

Current demonstrates how targeting specific demographics can drive exceptional growth in neobanking. By focusing on youth and family banking—a segment often overlooked by traditional banks—the company has built innovative features like instant gas station refunds and teen banking controls that create strong customer loyalty and viral adoption among younger users.

Series: $200 million (2024) from Andreessen Horowitz, Wellington Management, General Catalyst, and Cross River.

WeBank is China's first digital-only bank, serving over 300 million customers with micro-lending, wealth management, and digital banking services through integration with the WeChat ecosystem. Backed by Tencent, the Shenzhen-based company leverages AI-driven facial recognition and big data analytics for credit decisioning and service delivery.

WeBank represents the massive scale possible in digital banking when combined with ecosystem integration. By leveraging Tencent's WeChat platform, the company has achieved unprecedented customer penetration in China while providing financial services to previously unbanked populations through innovative AI-driven underwriting. This model demonstrates how platform integration can accelerate fintech adoption.

Backed by Tencent as licensed digital bank. Specific funding details not publicly disclosed; operates profitably at scale.

SoFi has evolved from a student loan refinancer into a diversified financial services platform offering banking, investing, lending, and insurance products. The San Francisco-based company serves 7 million members with a comprehensive suite of financial products designed to meet customers' needs across different life stages.

SoFi demonstrates how diversification can create sticky customer relationships and sustainable revenue streams in neobanking. By offering a comprehensive suite of financial products—from student loans to investing to banking—the company increases customer lifetime value while reducing churn through integrated service delivery. Its 2022 bank charter acquisition enables direct FDIC insurance and expanded capabilities.

Publicly traded on NASDAQ (SOFI). Full bank charter acquired in 2022 enabling expanded lending and FDIC insurance capabilities.

Starling Bank focuses on small business and SME banking, serving 3 million customers with business accounts, lending, and financial management tools. The London-based company has achieved profitability by specializing in SME services while also offering personal banking products to create a comprehensive financial platform.

Starling Bank proves that specialization in SME banking can drive profitability and sustainable growth in neobanking. The company's proprietary banking platform "Engine"—which can be licensed to other banks—creates an additional B2B revenue stream, demonstrating how neobanks can evolve beyond consumer banking into platform businesses that serve other financial institutions.

Achieved break-even in October 2020. Has not required additional external funding due to sustainable business model with strong SME lending cash flow.

N26 operates as a full-service digital bank across 24 European markets, offering banking, savings, and premium services with sleek design and sophisticated functionality. The Berlin-based company holds a full EU banking license, enabling comprehensive banking services across its operating markets.

N26 represents European neobanking excellence with its combination of regulatory compliance, design sophistication, and cross-border capabilities. The company's full EU banking license provides a competitive advantage over partnership-based models, while its premium metal card offerings attract young professionals and frequent travelers seeking elevated banking experiences.

Maintains $3 billion valuation. Has not disclosed recent funding rounds while expanding operations across Europe and into US/Brazil markets.

Varo Bank made history as America's first consumer fintech to receive a national bank charter, serving customers with fee-free banking, overdraft protection, and credit-building products. The company focuses on financial inclusion by providing banking services to traditionally underbanked communities.

Varo Bank's historic achievement in receiving a national bank charter validates the regulatory compliance and business model strength required for sustainable neobanking in the US. The charter eliminates dependence on partner banks and enables direct FDIC insurance, providing a competitive advantage in trust and regulatory positioning that few US neobanks have achieved.

Series D: $500 million+ raised at $2.5+ billion valuation while building chartered banking operations with direct FDIC insurance.

The neobanking market demonstrates several key trends that have direct implications for B2B go-to-market strategies:

Vertical Specialization Drives Growth: Companies like Mercury (startups), Starling (SMEs), and Current (youth) prove that targeting specific customer segments with tailored solutions creates stronger product-market fit and faster growth than horizontal banking approaches.

Geographic Focus Enables Market Dominance: Regional champions like Nubank (Latin America), Revolut (Europe), and KakaoBank (South Korea) achieve market leadership by deeply understanding local regulatory environments, consumer preferences, and distribution channels.

Profitability Requires Diversification: The most successful neobanks have diversified beyond basic banking into lending, investments, insurance, and other revenue streams. Revolut's super-app model and SoFi's multi-product approach demonstrate how revenue diversification drives sustainable profitability.

AI and Data Create Competitive Advantages: From WeBank's AI-driven credit scoring to Bunq's generative AI assistant, companies leveraging advanced AI and data analytics can deliver superior customer experiences and operational efficiency.

For B2B companies selling to or partnering with neobanks, these trends suggest the importance of precise audience targeting. Platforms like Landbase's natural-language targeting enable companies to identify decision-makers at specific neobank segments—for example, "CFOs at profitable neobanks with $1B+ revenue" or "CTOs at AI-focused neobanks in Europe."

For B2B companies looking to sell to or partner with fast-growing neobanks, success requires precise audience identification based on specific growth signals and characteristics. Here's how to approach this systematically:

1. Focus on Growth Signals: Target neobanks showing specific growth indicators like recent funding, rapid customer acquisition, geographic expansion, or new product launches. Landbase's real-time tracking can identify these signals automatically.

2. Segment by Business Model: Differentiate between profitability leaders (Nubank, Revolut, Monzo), hypergrowth challengers (Mercury, Current, Neo Financial), and specialized players (Starling for SMEs, Mercury for startups). Each requires different value propositions and engagement strategies.

3. Leverage Geographic Targeting: Consider regional regulatory environments and market characteristics when targeting neobanks. European neobanks with banking licenses have different needs than US neobanks operating through partnerships.

4. Identify Key Decision-Makers: Use AI-qualified discovery to find specific roles like CFOs at funded neobanks, CTOs at AI-focused neobanks, or CMOs at neobanks expanding into new markets.

5. Monitor Ecosystem Partnerships: Track neobanks' technology stack changes, partnership announcements, and integration needs to identify optimal timing for engagement.

Platforms like Landbase enable this precision targeting through natural-language prompts that can instantly identify relevant prospects based on these criteria, delivering AI-qualified audiences ready for immediate activation in existing sales and marketing tools.

Neobanks secure Series B funding by demonstrating strong product-market fit, sustainable unit economics, and clear paths to profitability or market dominance through proven customer retention and revenue per user metrics. Series B rounds typically range from $50-200 million and signal transition from product validation to scaling operations and geographic expansion. For example, Neo Financial's $68.5 million CAD round in January 2025 came after achieving #1 ranking on Canada's Top Growing Companies list, demonstrating the performance metrics required to attract institutional capital at this stage.

CEOs significantly impact neobank trajectories through strategic vision, regulatory navigation, and operational execution across multiple dimensions. David Vélez's focus on financial inclusion enabled Nubank's massive Latin American scale by addressing underbanked populations, while Nik Storonsky's super-app strategy drove Revolut's diversified revenue streams and four years of profitability. CEO leadership in navigating complex regulatory challenges—like Varo's historic US bank charter achievement or SoFi's 2022 charter acquisition—can create lasting competitive advantages that fundamentally differentiate business models. The CEO's ability to balance growth with profitability determines long-term sustainability in this competitive market.

AI and banking technology are fundamental to neobank success, enabling automated underwriting like WeBank's credit scoring, personalized user experiences through Bunq's Finn AI assistant, sophisticated fraud detection, and operational efficiency at scale. These technologies reduce operational costs by 30-50% compared to traditional banks while improving customer experience through instant decisions and 24/7 service availability. AI-driven credit assessment allows neobanks to serve previously underbanked populations by analyzing alternative data sources beyond traditional credit scores.

Neobanks face the same core banking regulations as traditional banks but often operate through different structural models that affect their regulatory requirements. Some neobanks like Varo and SoFi have obtained full banking charters enabling direct FDIC insurance and independent operations under comprehensive federal oversight. Others operate through partnerships with chartered banks, providing regulatory compliance through their partner while maintaining operational flexibility. The charter versus partnership distinction significantly impacts business model flexibility, direct customer relationships, lending capabilities, and competitive positioning. Full charters provide regulatory advantages but require substantial capital and compliance infrastructure investments.

Tool and strategies modern teams need to help their companies grow.